Palantir Stock: Brutal Buy or Sell Verdict 2026

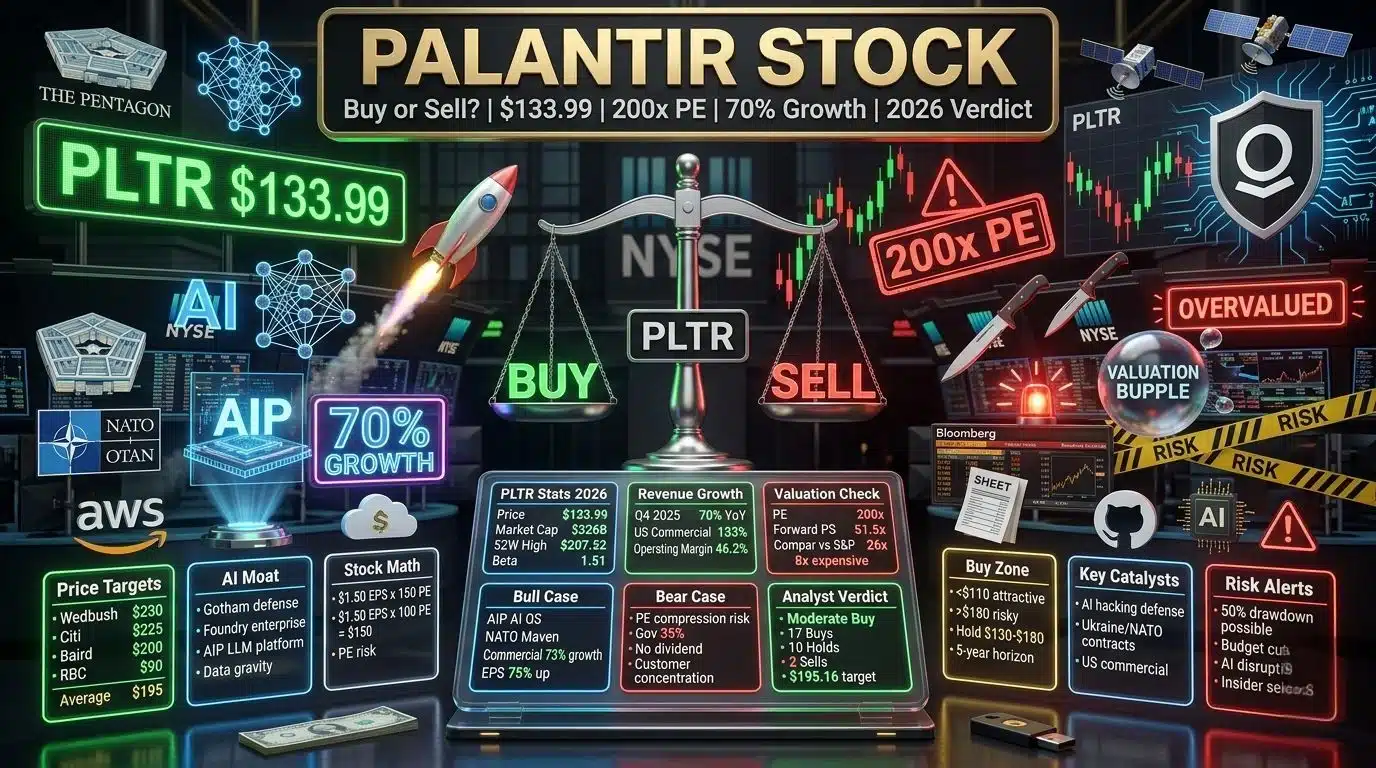

Palantir stock is up 545% in 5 years. It trades at $133.99 with a $326 billion market cap as of May 16, 2026. After 70% revenue growth in Q4 2025 and AI-driven demand, investors ask: is Palantir stock a buy now? The answer is brutal. Palantir stock has massive AI upside, sticky government contracts, and expanding commercial deals. But it also carries a 200x PE ratio, lumpy revenue, and heavy dependence on U.S. defense budgets. This guide breaks down the Palantir stock bull case, bear case, valuation, and 2026 price targets so you can decide.

Palantir Technologies builds data integration and AI decision platforms. Its Gotham, Foundry, and AIP products serve governments and Fortune 500 firms. After going public in 2020, Palantir stock became the poster child for AI software. It surged from $66.12 to $207.52 in 12 months. Now at $133.99, down 27% in 2026, the debate is hotter than ever. Palantir stock splits Wall Street.

Palantir Stock: Business Model and AI Moat

Understanding Palantir stock starts with the business. Palantir sells three core platforms:

- Gotham: For defense and intelligence. Used by U.S. military, NATO, and allies. Ukraine uses Gotham for AI-enabled battlefield ops. NATO awarded Palantir a contract for its Maven Smart System across 32 member states.

- Foundry: For commercial clients. Handles supply chain, finance, healthcare data. Walmart, Airbus, and BP use Foundry.

- AIP – Artificial Intelligence Platform: Launched 2023. Gives unified access to LLMs. Turns data into LLM objects and actions. AIP drove 70% growth in Q4 2025. U.S. commercial revenue jumped 133% YoY.

The Palantir stock moat is data gravity. Once clients load years of sensitive data into Gotham or Foundry, switching costs are extreme. Security, provenance, and real-time collaboration matter for governments. That keeps churn low. Palantir stock benefits from multi-year deals and $5M+ contracts. Top 20 customers account for nearly half of revenue.

Palantir Stock: Financial Performance 2026

Palantir stock is backed by accelerating numbers:

| Metric | Q4 2025 | FY 2025 | 2026 Trend |

|---|---|---|---|

| Total Revenue | $1.18B | $4.2B | 70% YoY Growth |

| Government Revenue | $633M | $2.3B | 55% YoY Growth |

| Commercial Revenue | $548M | $1.9B | 73% YoY Growth |

| Operating Margin | 46.2% | 38% | Expanding |

| Customer Count | 954 | 954 | +30% YoY |

| US Commercial Growth | 133% YoY | 95% YoY | Accelerating |

Q1 FY26 revenue grew 84.7% with operating margin at 46.2%. Palantir stock revenue CAGR from 2020-2024 was 21.3%. The commercial business now outpaces government. In Q3 2025, commercial grew 81.8% annually. This diversification reduces risk for Palantir stok holders. The company beat EPS estimates by 15% average over the last six quarters.

Palantir : Valuation Reality Check

Here is where Palantir stok gets controversial. The numbers:

- Current Price: $133.99

- 52 Week Range: $115.01 to $207.52

- Market Cap: $326.03B

- P/E Ratio: ~200. Peak was 350 in August 2025.

- Forward P/S: 51.5x on 2026 estimates

- Forward P/E: 100x+

- Beta: 1.51. Palantir stock is volatile.

Palantir stock is priced for perfection. At 200x earnings, it is 8x more expensive than the S&P 500 at 26x. Wall Street expects $1.31 EPS in 2026, up 75%. Even if Palantir hits $1.50 EPS, a 150 PE gives $225 price. A 100 PE gives $150. If sentiment sours and PE compresses to 100, Palantir stok falls even on earnings growth.

Palantir : Bull Case for 2026

1. AI Operating System Narrative

Palantir is positioning AIP as the AI operating system for enterprises. Just as Microsoft dominated PCs and Apple owns mobile, Palantir stock bulls see it controlling AI workflows. If true, the TAM is $251B by 2033 growing 38% annually. Palantir stok is growing 70% now, faster than the market.

2. Government Moat Expanding

U.S. government is 35% of revenue. But it is sticky. Palantir won NATO Maven Smart System. UK, Germany, France, and Nordics are expanding. HD Hyundai partnership opens Asia. Defense modernization is not optional. Palantir stock wins regardless of administration.

3. Commercial Inflection

U.S. commercial grew 133% YoY. Deal sizes are larger and longer. Customers like BP and Airbus are standardizing on Foundry. AIP adoption compounds. This gives Palantir stock a second growth engine beyond defense.

4. Operating Leverage

Margins hit 46.2%. Software scales. Each new dollar of revenue drops more to profit. EPS growth of 75% in 2026 is possible. That helps Palantir stock grow into its valuation.

5. AI Hacking Tailwind

Google warns AI-assisted hacking is here. Zero-day exploits bypass 2FA. Governments and firms need Palantir’s AI defense tools. Cyber threats boost demand. Palantir stock is a picks-and-shovels AI security play.

Palantir Stock: Bear Case for 2026

1. Valuation Risk

Palantir stock trades at 200 PE. History says this is unsustainable. Even great companies like Nvidia and Microsoft saw 70-90% drawdowns. If growth slows, Palantir stok could crash. Motley Fool sees risk if PE drops to 100.

2. Customer Concentration

Top 20 customers are ~50% of revenue. If one major government shifts budget, Palantir stock revenue is lumpy. Defense contracts are political. Different administrations have different priorities.

3. AI Disruption Risk

Palantir is not AI-native. A startup built ground-up on LLMs could create a better solution. Open-source AI tools erode moats. Palantir stock must innovate fast.

4. Government Dependency

35%+ revenue from U.S. government. Budget cuts or procurement changes hit Palantir stock hard. The company is diversifying, but slowly.

5. No Dividends

Palantir stock pays no dividend. All return is from price appreciation. In a bear market, holders get no income.

Palantir : Wall Street Price Targets 2026

Analyst consensus on Palantir stock is “Moderate Buy” from 31 analysts:

- Strong Buy: 2

- Buy: 17

- Hold: 10

- Sell: 2

- Average Price Target: $195.16

- High Target: $230 (Wedbush)

- Low Target: $90 (RBC)

| Firm | Rating | Price Target |

|---|---|---|

| Wedbush | Outperform | $230.00 |

| Citigroup | Buy | $225.00 |

| Rosenblatt | Buy | $225.00 |

| Baird | Outperform | $200.00 |

| UBS | Buy | $200.00 |

| Mizuho | Outperform | $185.00 |

| DA Davidson | Neutral | $165.00 |

| RBC | Underperform | $90.00 |

Motley Fool predicts Palantir stok hits $200 by Dec 2026, +21% upside. At 150 PE and $1.50 EPS, price is $225. That implies 50% upside from $150. But if PE drops to 100, Palantir stok declines even with growth.

Palantir : Is It a Buy, Sell, or Hold?

The Palantir stock verdict depends on risk tolerance:

Read More: Protecting Bank Account from AI Deepfake Fraud: The 2026 Essential Guide

Buy Palantir Stock If:

- You believe AI is the next operating system and Palantir leads it.

- You can hold 5+ years through 50%+ volatility.

- You trust government contracts stay sticky.

- You think 70% growth continues and margins expand.

- You buy below $110 where valuation is 25x 2027 sales.

Hold Palantir Stock If:

- You own it already and believe in long-term AI adoption.

- You accept volatility and are not adding at 200 PE.

- You want exposure to defense + AI in one name.

Sell Palantir Stock If:

- You need capital in 12 months. Palantir stock can drop 50% fast.

- You believe AI spending is a bubble.

- You want dividends or value metrics.

- You think PE compression to 100 is likely.

My take: Palantir stok is a hold above $130. Start accumulating below $110. The business is elite. The price is not. Even the best companies see huge drawdowns. Nvidia, Alphabet, Apple, and Microsoft all fell 70%+ on their way up. Palantir stok will too.

Palantir : Key Risks to Watch

Before buying Palantir stock, monitor:

- Revenue Deceleration: If growth drops below 40%, PE will compress.

- Government Budget: Any defense cuts hit 35% of revenue.

- Competition: Snowflake, Databricks, and AI-native startups.

- Insider Selling: Alex Karp and execs sold stock in 2025.

- Market Sentiment: SaaS multiples collapsed in 2022. Could repeat.

Palantir : Long-Term Outlook

Palantir stock can become one of the largest AI companies. Companies controlling operating systems get massive. If AIP is the AI OS, $1T market cap is possible by 2035. But path is volatile. Palantir stok at 51.5x sales caps upside for 2-3 years as it grows into valuation.

Buy Palantir stock on dips, not chasing. Below $110 is attractive at 25x 2027 sales. Above $180, risk-reward skews negative. Palantir stok is a 10-year story, not 10-month trade.

FAQ Section

1. Why is Palantir stock so expensive?

Investors pay for 70% growth, 46% margins, and AI leadership. The market views it as the AI operating system. High growth + high margins = high multiple. But it leaves no room for error.

2. Does Palantir pay a dividend?

No. Palantir reinvests all cash into growth and R&D. Do not buy for income. Buy for capital appreciation.

3. Is Palantir only a government contractor?

No. Government was 100% at IPO. Now commercial is 45% and growing 73% YoY. U.S. commercial grew 133%. The business is diversifying fast.

4. What is AIP and why does it matter?

Artificial Intelligence Platform. It lets clients use LLMs on private data. It drove the recent growth inflection. AIP makes Palantir central to enterprise AI adoption.

5. Can Palantir stock reach $200 in 2026?

Yes, per Wedbush and Baird. Needs $1.50 EPS and 150 PE, or continued AI hype. If growth slows or market drops, $200 is unlikely.

6. What is the biggest risk to Palantir?

Valuation. At 200 PE, any miss causes 30-50% drop. Customer concentration and government budget risk are also major.

7. Is Palantir profitable?

Yes. Operating margin is 46.2% in Q1 FY26. Net income positive. It generates free cash flow. Unlike many 2021 IPOs, Palantir makes money.

8. Should I buy Palantir before earnings?

Risky. Stock moves 10%+ on earnings. It beat estimates 6 straight quarters. But expectations are high. Consider small position and add on dips.

Meet Md. Rubel Rana

As a core contributor to Worlddincidents.com, Rubel Rana brings a unique perspective to the world of journalism. Whether it’s deep-diving into historical trivia or covering the latest global headlines, Rubel Rana is committed to delivering high-quality, high-impact articles. Their writing blends meticulous research with a compelling voice, helping readers stay informed and curious about the world around them.