College Payment: 9 Proven Ways to Fund Your Degree 2026

Confused about which are ways to pay for a college education? You are not alone. With 2026-27 tuition at public colleges averaging $11,000 in-state and private schools hitting $80,000, finding the right college payment strategy is critical. Between FAFSA, grants, loans, and scholarships, the options feel endless. This guide breaks down 9 proven methods for college payment so you can combine free money, earned income, and smart borrowing without drowning in debt.

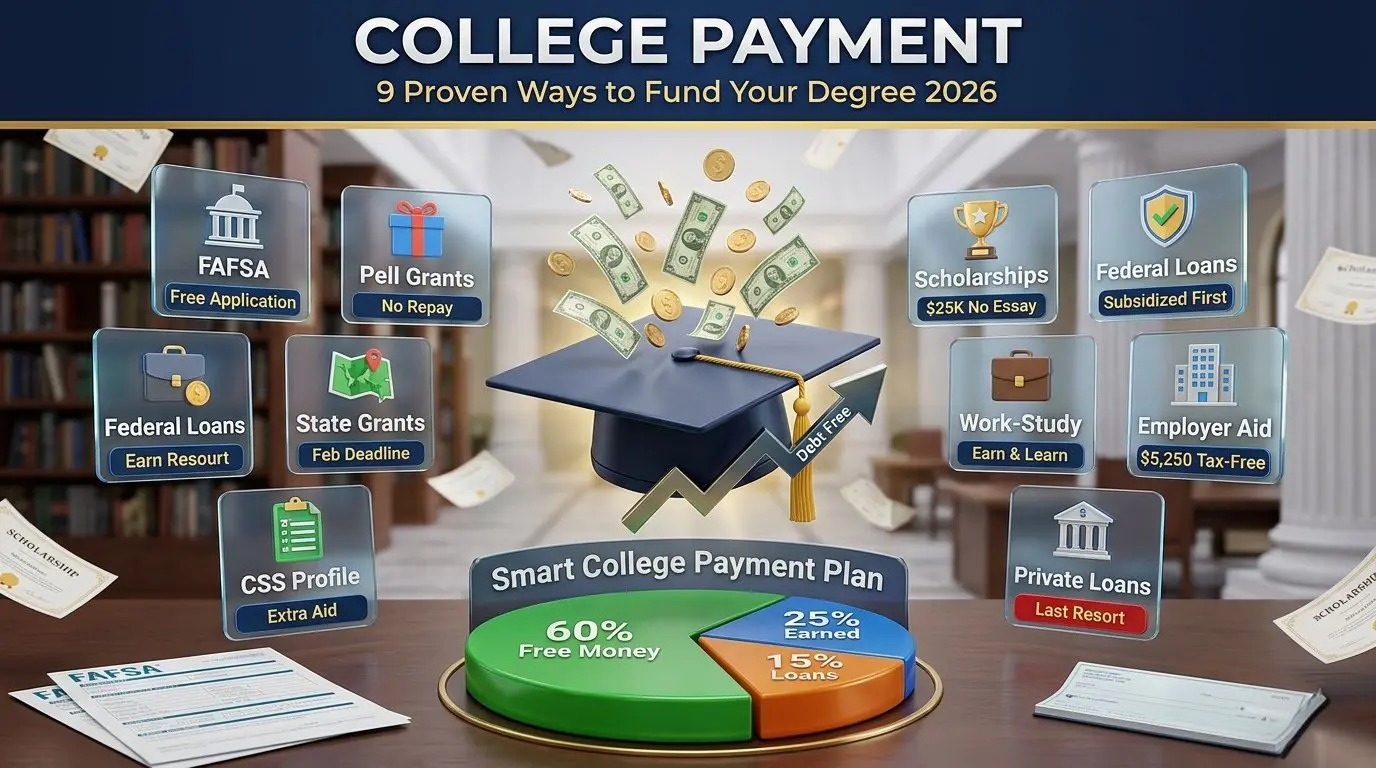

The best college payment plan uses free aid first, earned money second, and loans last. For 2026, the FAFSA opened September 24, 2025 and state deadlines hit February-April 2026. Many funds are first-come, first-served. Start your college payment research 12-18 months early to maximize aid.

Read More: Fanless Laptops 2026: Ultimate Silent Picks for Work & Study

1. File the FAFSA: Your Gateway to All Federal College Payment Aid

The Free Application for Federal Student Aid is non-negotiable if you want financial help. The 2026-27 FAFSA opened September 24, 2025. Federal deadline is June 30, 2027, but state and school priority deadlines are February-April 2026. File early because state grants run out.

There is no income cutoff for FAFSA. A family earning $120,000 can still get federal student loans, institutional grants, merit scholarships, state aid, and work-study. At high-cost schools, even six-figure earners can demonstrate financial need. Families over $400,000 likely get unsubsidized loans and merit aid only, but should still file. It costs nothing and takes an hour.

FAFSA determines eligibility for Pell Grants, FSEOG, Direct Subsidized Loans, Unsubsidized Loans, PLUS Loans, and Work-Study. This is step one for any college payment plan.

2. Pell Grants and FSEOG: Free College Payment You Keep

Federal Pell Grants are need-based and awarded to undergraduate students with exceptional financial need. You do not repay them. For 2026, Pell Grants remain the foundation of need-based college payment. Around 84% of students receive financial aid through need-based grants.

Federal Supplemental Educational Opportunity Grants or FSEOG are also need-based for undergrads, with priority to Pell recipients. State grants work similarly. Combined, grants are the best college payment because they are free money. Check your state’s deadline. Many are in February 2026.

3. Scholarships: Merit-Based College Payment That Does Not Need Repayment

Scholarships are free college payment awarded for merit, talent, demographics, or need. You do not repay them. For 2026, there are 300+ active opportunities.

Top No-Essay Scholarships 2026

- Scholarships360 $10,000 No Essay: Open to all grade levels. Deadline June 30, 2026. Apply monthly for better odds.

- Niche $25,000 No Essay: High school and college students. Deadline May 31, 2026. Random drawing.

- Sallie $2,000 Monthly: Deadline April 30, 2026. No essay or sign-ups.

Institutional Scholarships

Colleges offer their own merit aid. Examples for 2026: WGU Arizona Partnership $4,000, Colorado Roy Romer $4,000, Maryland Rising Together $4,000, Gianforte Montana $5,000. All have June 30, 2026 deadlines. Many schools require FAFSA for any institutional aid, even merit.

Scholarship Stacking

You can combine federal, state, institutional, and private scholarships. Total aid cannot exceed Cost of Attendance. If you get too much, schools reduce loans first, then work-study. Pell Grants are protected and reduced last. Smart stacking is key to a debt-free college payment plan.

4. Federal Student Loans: Best Borrowing Option for College Payment

When free money is not enough, federal loans fill the gap. They have fixed rates and forgiveness options, making them the safest college payment loan.

Types of Federal Loans

- Direct Subsidized Loans: For undergrads with financial need. Interest does not accrue while enrolled at least half-time, in deferment, or grace period.

- Direct Unsubsidized Loans: For undergrad and graduate students. No need requirement. Interest accrues immediately.

- Direct PLUS Loans: For grad students and parents. Cover cost beyond other aid.

Subsidized loans are the best college payment debt because the government pays interest while you study. Borrow subsidized first, then unsubsidized.

5. Private Student Loans: Last Resort College Payment

Private loans have higher rates and no forgiveness. Use only after maxing federal aid. They should be your last choice for college payment. Terms vary by credit score and lender. Always compare APR, not just monthly payment.

6. Federal Work-Study: Earn Your College Payment

Work-study lets you earn money while in school. It is need-based and part of your FAFSA award. Jobs are often on campus and tied to your major. This college payment is earned, not borrowed, so no debt. However, it is not guaranteed until you work the hours. List it in your award letter as earned money.

7. Employer Tuition Reimbursement: Tax-Free College Payment

Under IRS Section 127, employers can give up to $5,250 per year tax-free for education. You pay no income tax on it. It covers tuition, fees, books, supplies. Courses do not need to be job-related. Many companies offer this but do not advertise it. Check HR. This is free college payment many employees overlook.

8. State and Third-Party Programs

Many states offer grants separate from federal aid. Deadlines are often February-April 2026. Community colleges like Tri-C offer scholarships, work-study, and loans. Third-party sponsors can also pay directly to schools. Ask your college’s financial aid office what state and local college payment options exist.

9. Service and Special Circumstance Scholarships

Service scholarships reward community work or family service. Examples: children of police, firefighters, EMTs, military. Veteran programs include PVA Scholarship $1,000-$2,500, Gruber $2,000, and CTU Patriot full tuition. There are also scholarships for people with felonies, past-due tuition, and teaching majors like the TEACH Grant and AMS Teacher Education Scholarship. These targeted awards can be a major college payment source.

How to Build Your 2026 College Payment Plan

Follow this order to minimize debt:

- Free Money: FAFSA > Pell/FSEOG > State Grants > Institutional Scholarships > Private Scholarships

- Earned Money: Work-Study > Employer Reimbursement > Part-time job

- Borrowed Money: Subsidized Federal Loans > Unsubsidized Federal > PLUS > Private Loans

Start 12-18 months early. Spring 2025: research schools with Net Price Calculators and hunt scholarships. October 1, 2025: file FAFSA ASAP. January-March 2026: meet state and school deadlines. Submit CSS Profile if required.

Reading Award Letters: Spot Real College Payment vs Loans

Colleges sometimes list loans as “awards” to look generous. Break down your package:

- Keep: Pell, FSEOG, state grants, scholarships

- Pay Back: Subsidized, Unsubsidized, PLUS, Private loans

- Earn: Work-study

Ask: Is tuition final for 2026-27? Public colleges often finalize rates after aid is sent. Will aid renew all four years? Check GPA and credit requirements. If aid is insufficient, ask about appeals and emergency funding. This protects your college payment plan from surprises.

Common College Payment Mistakes to Avoid

1. Not filing FAFSA: Even high-income families get unsubsidized loans and may need it for merit aid.

2. Missing state deadlines: February 2026 for many states. File in October 2025.

3. Confusing loans with grants: Loans are debt. Grants are free.

4. Borrowing too much: Student debt affects life after graduation. Borrow responsibly.

5. Ignoring employer aid: $5,250 tax-free is huge. Ask HR.

FAQ Section

1. Do I need to pay back a Pell Grant?

No. Pell Grants are need-based federal aid that you do not repay unless you withdraw early or your eligibility changes.

2. What is the FAFSA deadline for 2026-27?

Federal deadline is June 30, 2027. But state and school priority deadlines are February-April 2026. File as early as possible after September 24, 2025.

3. Can I get financial aid if my parents make $400,000?

You likely will not get need-based aid like Pell or subsidized loans. But you can still get unsubsidized loans and merit scholarships. Some schools require FAFSA for any aid.

4. What is the difference between subsidized and unsubsidized loans?

Subsidized loans are for students with need. The government pays interest while you are in school. Unsubsidized loans accrue interest immediately for all students.

5. How many scholarships can I combine?

You can stack federal, state, institutional, and private scholarships. Total aid cannot exceed Cost of Attendance. If over, schools cut loans first, then work-study.

6. Is work-study guaranteed money?

No. It is earned through a job. The award shows maximum you can earn, but you must work the hours.

7. Does employer tuition help cover any degree?

Yes. Under IRS Section 127, up to $5,250 per year is tax-free and does not need to be job-related. Check your HR policy.

8. Are online students eligible for financial aid?

Yes. Around 84% of online students receive aid including Pell, FSEOG, and federal loans. File FAFSA to determine eligibility.

Meet Md. Rubel Rana

As a core contributor to Worlddincidents.com, Rubel Rana brings a unique perspective to the world of journalism. Whether it’s deep-diving into historical trivia or covering the latest global headlines, Rubel Rana is committed to delivering high-quality, high-impact articles. Their writing blends meticulous research with a compelling voice, helping readers stay informed and curious about the world around them.

1 thought on “College Payment: 9 Proven Ways to Fund Your Degree 2026”